VA Home Loans: Easy Tips to Qualify and Apply for Expert Perks

VA Home Loans: Easy Tips to Qualify and Apply for Expert Perks

Blog Article

Optimizing the Conveniences of Home Loans: A Detailed Strategy to Securing Your Ideal Home

Browsing the complex landscape of home loans requires a systematic method to ensure that you safeguard the property that lines up with your financial objectives. To really make the most of the advantages of home fundings, one must consider what steps follow this fundamental job.

Comprehending Mortgage Basics

Recognizing the principles of mortgage is crucial for any person thinking about acquiring a building. A home financing, commonly referred to as a mortgage, is a monetary product that allows people to borrow cash to purchase real estate. The customer accepts pay off the car loan over a defined term, usually ranging from 15 to three decades, with passion.

Key parts of home mortgage include the principal amount, rates of interest, and repayment timetables. The principal is the quantity obtained, while the interest is the expense of borrowing that quantity, expressed as a percent. Rates of interest can be fixed, staying constant throughout the loan term, or variable, changing based upon market conditions.

Furthermore, consumers ought to be aware of numerous types of home loans, such as traditional loans, FHA finances, and VA finances, each with distinct eligibility standards and benefits. Recognizing terms such as down repayment, loan-to-value proportion, and private mortgage insurance coverage (PMI) is additionally crucial for making notified choices. By grasping these fundamentals, prospective property owners can navigate the intricacies of the home mortgage market and recognize options that align with their financial objectives and building aspirations.

Assessing Your Financial Situation

Assessing your monetary circumstance is a critical step before embarking on the home-buying trip. This analysis entails a comprehensive evaluation of your earnings, expenses, savings, and existing debts. Begin by calculating your overall monthly revenue, consisting of incomes, bonuses, and any kind of extra sources of income. Next, checklist all month-to-month costs, ensuring to account for fixed prices like lease, utilities, and variable expenditures such as groceries and home entertainment.

After establishing your revenue and costs, determine your debt-to-income (DTI) proportion, which is necessary for loan providers. This ratio is computed by dividing your complete monthly financial debt repayments by your gross monthly earnings. A DTI ratio below 36% is usually thought about favorable, showing that you are not over-leveraged.

Furthermore, assess your credit rating, as it plays a critical duty in safeguarding beneficial financing terms. A higher credit report can cause reduced rates of interest, inevitably conserving you money over the life of the funding.

Discovering Financing Alternatives

With a clear image of your financial scenario developed, the following step includes discovering the different funding choices offered to prospective property owners. Recognizing the various kinds of home fundings is vital in choosing the appropriate one for your needs.

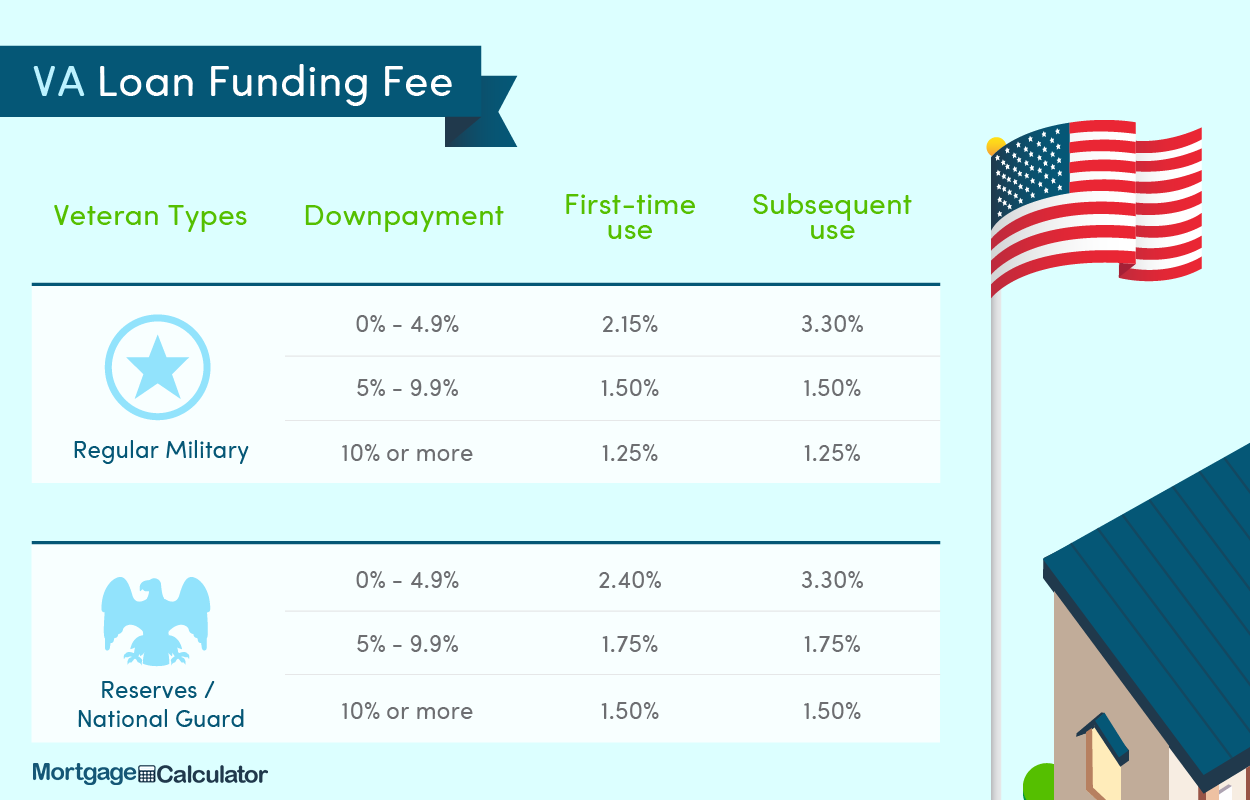

Standard loans are standard financing methods that usually call for a greater credit report and deposit yet offer affordable rates of interest. Alternatively, government-backed finances, such as FHA, VA, and USDA financings, provide to particular teams and typically require reduced deposits and credit report, making them obtainable for novice customers or those with restricted funds.

An additional option is variable-rate mortgages (ARMs), which feature reduced first rates that adjust after a specific duration, possibly causing substantial savings. Fixed-rate home loans, on the other hand, supply security with a constant rate of interest throughout the finance term, protecting you versus market variations.

In addition, consider the lending term, which usually ranges from 15 to thirty years. Much shorter terms might have higher monthly settlements but can save you rate of interest with time. By carefully examining these alternatives, you can make an informed decision that lines up with your monetary objectives and homeownership desires.

Preparing for the Application

Successfully preparing for the her comment is here application process is vital for protecting a home lending. A solid credit rating rating is essential, as it influences the finance quantity and passion prices offered to you.

Next, collect essential paperwork. Common requirements consist of current pay stubs, income tax return, financial institution declarations, and proof of properties. Organizing these papers beforehand can considerably expedite the application procedure. Furthermore, consider acquiring a pre-approval from lenders. This not just supplies a clear understanding of your borrowing capability but also reinforces your setting when making a deal on a residential property.

Moreover, establish your budget plan by considering not simply the financing amount however additionally residential property taxes, insurance coverage, and maintenance costs. Familiarize yourself with different financing types and their respective terms, as this understanding will encourage you to make enlightened choices throughout the application procedure. By taking these proactive steps, you will certainly improve your readiness and enhance your possibilities of safeguarding the home mortgage that finest fits your needs.

Closing the Offer

During the closing conference, you will assess and authorize different files, such as the loan quote, closing disclosure, and home loan agreement. It is vital to thoroughly comprehend these documents, as they detail the car loan terms, settlement schedule, and closing expenses. Take the time to ask your lending institution or real estate representative any concerns you might need to avoid misconceptions.

Once all files are authorized and funds are transferred, you will receive the tricks to your brand-new home. Remember, shutting prices can vary, so be gotten ready for expenditures that might include evaluation costs, title insurance, and attorney charges - VA Home Loans. By remaining arranged and informed throughout this process, you can make sure a smooth change right into homeownership, taking full advantage of the advantages of your home financing

Final Thought

Finally, making the most of the advantages of mortgage requires a methodical strategy, incorporating an extensive analysis of economic conditions, expedition of varied lending go options, and careful prep work for the application process. By adhering to these steps, potential house More Info owners can enhance their possibilities of protecting beneficial funding and attaining their home possession objectives. Inevitably, cautious navigation of the closing process further solidifies an effective transition right into homeownership, making certain lasting economic stability and fulfillment.

Navigating the facility landscape of home car loans requires a methodical strategy to make sure that you protect the home that straightens with your monetary objectives.Recognizing the basics of home car loans is essential for anyone thinking about buying a home - VA Home Loans. A home finance, typically referred to as a home loan, is a financial product that allows people to obtain money to acquire real estate.In addition, debtors must be aware of different types of home lendings, such as conventional finances, FHA financings, and VA finances, each with distinct eligibility standards and benefits.In conclusion, maximizing the advantages of home car loans requires an organized strategy, incorporating a complete evaluation of economic scenarios, exploration of diverse car loan options, and meticulous prep work for the application procedure

Report this page